What to Know

- BIS General Manager Pablo Hernández de Coswarned on Monday in Japan that the slowdown in international rulemaking risks a damaging patchwork of regimes

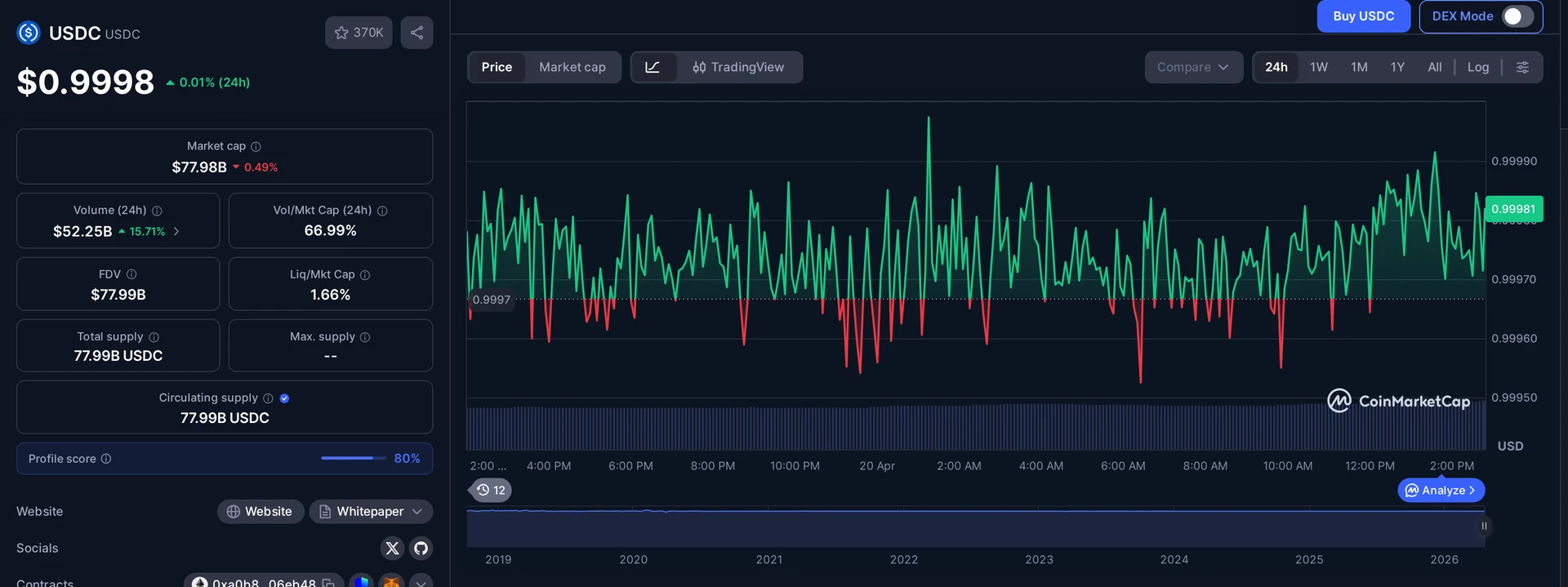

- Thestablecoin markethas swelled to$320 billionwithTether’s USDTandCircle’s USDCholding the lion’s share of that float

- Bank of England Governor Andrew Baileywho chairs the Financial Stability Board, said progress on global stablecoin standards has stalled over the past year

- TheDigital Asset Market Clarity Actis before theU.S. Senateafter passing the House last year, with a markup possibly landing in the second half of April

Global stablecoin standards are stuck. That is the blunt message from the world’s biggest central bank for central banks, and it landed this week with the kind of urgency you do not usually hear out of Basel. Speaking in Japan on Monday,Bank for International SettlementsGeneral Manager Pablo Hernández de Cos warned that a year of drift on cross-border rulemaking has left regulators exposed to the one thing they dread most: a fragmented regime that clever firms can route around at will. Behind his warning sits a number that keeps growing while the rulebook sits still.$320 billion.

Bank for International Settlements Chief Says the Rulebook Is Falling Behind the Money

De Cos did not sugarcoat it. Progress on international coordination has slowed over the past year, he told an audience in Japan, and the longer that drift continues, the more room firms have to exploit the gaps between jurisdictions. That practice has a name in the regulator’s lexicon: regulatory arbitrage. It is the quiet migration of activity from places with strict oversight to places with lighter touch, and it has a long track record of ending badly.

The warning was not delivered in a vacuum.Bank of England Governor Andrew Baileywho also chairs the Financial Stability Board, said last week thatglobal stablecoin standardshave stalled. When the two most senior voices in international financial plumbing sing from the same hymn sheet within a week of each other, that is not a coincidence. That is a coordinated nudge.

The nudge is aimed at national regulators, not the industry. Washington, Brussels, Tokyo, and London are all writing their own playbooks on different timelines, with different definitions of what a stablecoin even is. A token that counts as a payment instrument in one capital may be treated as a security in the next. For a$320 billionmarket that settles across borders in seconds, that mismatch is not a detail. It is the whole ballgame.

Without international alignment, companies may shift operations to jurisdictions with lighter oversight.

How Big Is the Stablecoin Market Right Now?

It is big enough to matter, and growing faster than most central banks can process. Thestablecoin marketsits around$320 billionin total supply, according to DeFiLlama data. Tether’sUSDTand Circle Internet’sUSDCaccount for the bulk of that figure, with a long tail of smaller issuers making up the rest.

Put that number next to traditional finance and it starts to feel less like a crypto curiosity.$320 billionis larger than the GDP of most countries. It is larger than some of the biggest money market funds in the United States. And unlike money market funds, a meaningful slice of that balance moves on public blockchains in transactions that clear in minutes, not days.

That is the supply side. The flow side is even harder to wave away. Stablecoins now settle trillions of dollars in annual volume, a big chunk of it outside the U.S. banking perimeter entirely. When de Cos argued on Monday that sudden withdrawals could ripple through markets, he was not floating a hypothetical. He was describing a plumbing problem that already has scale.

- Total supply: around$320 billionacross all issuers

- Market leaders:Tether’s USDTandCircle’s USDChold most of the float

- Primary use cases: crypto trading collateral, cross-border payments, dollar access in emerging markets

- Primary regulatory concern: redemption frictions that can push prices away from the$1peg

Why De Cos Thinks Stablecoins Look More Like Securities

The most pointed line in the BIS chief’s speech was not about rulemaking timelines. It was about what these things actually are. De Cos said the structure of major stablecoins can resemble securities more than cash. That is a loaded sentence, and every word of it earns its keep.

His reasoning goes like this. A cash equivalent redeems at par, instantly, without friction. A stablecoin does not always do that. Redemption frictions, whether from queues, gating, or reserve composition, can push the secondary-market price away from its intended$1value. When that happens, holders are no longer sitting on a dollar. They are sitting on a claim on a dollar, priced by a market, exactly like a short-duration security.

That distinction is not academic. If regulators accept the securities-like framing, the policy toolbox shifts. Suddenly you are talking about reserve transparency rules, redemption guarantees, and circuit breakers, not just anti-money-laundering checks. You are also talking about who gets to issue, and under which license.

Redemption frictions can push prices away from their intended one-dollar value, and sudden withdrawals could ripple through markets.

How Global Stablecoin Standards Could Get Fixed: Yield Caps and Backstops

De Cos did not just catalogue risks. He pointed at two proposals that keep coming up in international discussions and both would reshape the economics of the business. The first is limiting interest payments on stablecoins. That would kneecap the yield-bearing product category that issuers have been inching toward for two years, the one that turns a payment token into something closer to a money market share.

The second proposal is harder to dismiss as hostile. It would give stablecoin issuers access to central bank lending facilities or deposit-insurance-style arrangements. In plain terms, it would fold the biggest issuers into the official safety net the way banks already are. That sounds friendly until you read the fine print, because access to the safety net always comes with strings attached: capital rules, liquidity rules, examiner visits, and a much narrower definition of what counts as a reserve asset.

Call it pragmatism or call it regulatory capture of a new asset class, the direction of travel is clear. Policymakers want these tokens to behave less like free-range fintech and more like regulated narrow banks. The industry’s pushback has been measured so far, but the margin compression implicit in these proposals is real. Ban yield on the liability side and require central bank eligible reserves on the asset side, and the business model that made Tether one of the most profitable companies per employee on Earth starts to look very different.

Where the U.S. Senate Fight Actually Stands

The United States is the variable everyone is watching, because the dollar is the currency under every major stablecoin hood. TheDigital Asset Market Clarity Actpassed the House last year and now sits in the Senate, where the political math is tighter than the bill’s supporters like to admit. Banking Committee ChairmanTim Scottand Agriculture Committee ChairmanJohn Boozmanare pushing it forward. SenatorsThom TillisandAngela Alsobrookshammered out a compromise on stablecoin yield that could open the door to a markup.

SenatorCynthia Lummiswho chairs the Banking Committee’s digital assets subcommittee, floated a hearing in the second half of April. Whether that hearing actually happens on schedule is a separate question. Several open items still need resolving, including how the bill treats decentralized finance and what ethics provisions get attached, the sort of plumbing fights that have killed crypto legislation before.

Here is the part that matters for the fragmentation argument de Cos raised on Monday. If the Senate moves, the U.S. sets a de facto global benchmark whether Basel likes it or not, because issuers will align with the biggest dollar market on Earth. If the Senate stalls, every other jurisdiction writes its own rules first, and the patchwork the BIS is warning about becomes permanent. The clock is not neutral. Every month without a U.S. framework is a month other capitals set precedent.

- Tim ScottSenate Banking Committee Chairman, leading the push

- John BoozmanSenate Agriculture Committee Chairman, co-leading

- Thom TillisandAngela Alsobrooksbrokered the compromise on stablecoin yield

- Cynthia Lummisdigital assets subcommittee chair, floated an April hearing

What Does This Mean for Holders and Issuers?

Short answer: more rules are coming, and the only real question is whose rules win. For holders ofUSDTandUSDCthe practical impact of a global standard would likely be tighter reserve disclosures, clearer redemption rights, and in some scenarios a cap on any yield that is paid directly on the token. None of that changes how stablecoins function as payment rails tomorrow morning. All of it changes how the issuers make money five years from now.

For issuers, the calculus is already shifting. Circle has leaned into regulated status and listed its shares under the tickerCRCLa bet that proximity to the official sector is an asset, not a liability. Tether has taken the opposite tack, keeping its headquarters and its reserve composition as lean as the market will tolerate. A unified global standard would force both models to converge, probably toward Circle’s end of the spectrum. That is good news for the regulated camp and a structural headwind for anyone built around opacity.

The wild card is whether regulators can actually deliver the coordination the BIS is calling for. History says probably not, or at least not quickly. Basel III took years to negotiate and more years to implement, and that was for banks that already had a shared vocabulary. Stablecoins do not. The industry and the central banks do not even fully agree on what these instruments are. De Cos is right to sound the alarm. He is also, almost certainly, going to be sounding it for a while.

Frequently Asked Questions

What did the BIS say about global stablecoin standards?

BIS General Manager Pablo Hernández de Cos said on Monday in Japan that international stablecoin rulemaking has slowed and warned that the lack of coordination risks producing a patchwork of rules firms could exploit through regulatory arbitrage, shifting operations to lighter-touch jurisdictions.

How large is the stablecoin market in 2026?

The stablecoin market stood at roughly $320 billion in total supply as of April 2026, according to DeFiLlama data. Tether’s USDT and Circle’s USDC account for the majority of that figure, with a long tail of smaller dollar and euro-denominated issuers making up the remainder of the float.

Why does BIS say stablecoins resemble securities more than cash?

Pablo Hernández de Cos argued that redemption frictions can push stablecoin prices away from their intended $1 value, meaning holders carry a claim priced by a market rather than a true dollar equivalent. That structural behavior, he said, looks closer to a short-duration security than to cash.

What is the Digital Asset Market Clarity Act?

The Digital Asset Market Clarity Act is U.S. legislation that would create a federal framework for digital asset markets, including stablecoins. It passed the House in 2025 and is now before the Senate, where Banking Chair Tim Scott and Agriculture Chair John Boozman are leading the effort toward a markup.

This article is for informational purposes only and does not constitute investment advice. Every investment and trading decision involves risk. Readers should conduct their own research before making any financial decisions.

BIS has been sounding this alarm since the Libra days and the coordination problem only gets worse. FSB published recommendations in 2023 and jurisdictions still diverge on reserve composition and redemption rights.

stalled is generous. MiCA is live in the EU, the GENIUS bill is stuck in committee, Singapore and HK have their own frameworks. there is no common standard because nobody wants to cede first mover advantage

$320B market cap and USDT alone clears more volume than Visa on some days. regulators showing up a decade late as usual

Curious what readers think: does BIS actually have leverage here or is this just a speech cycle before Basel meetings?

fragmentation is a feature for issuers, not a bug.