What to Know

- The Financial Conduct Authority raided eight UK locations linked to illegal peer-to-peer crypto trading on Wednesday

- Zero peer-to-peer crypto traders or platforms are currently registered with the regulator under AML rules

- Operators received cease-and-desist notices on site while HMRC and the South West Regional Organised Crime Unit gathered evidence

- The incoming FSMA crypto regime takes effect in 2027, with authorization applications opening in September 2026

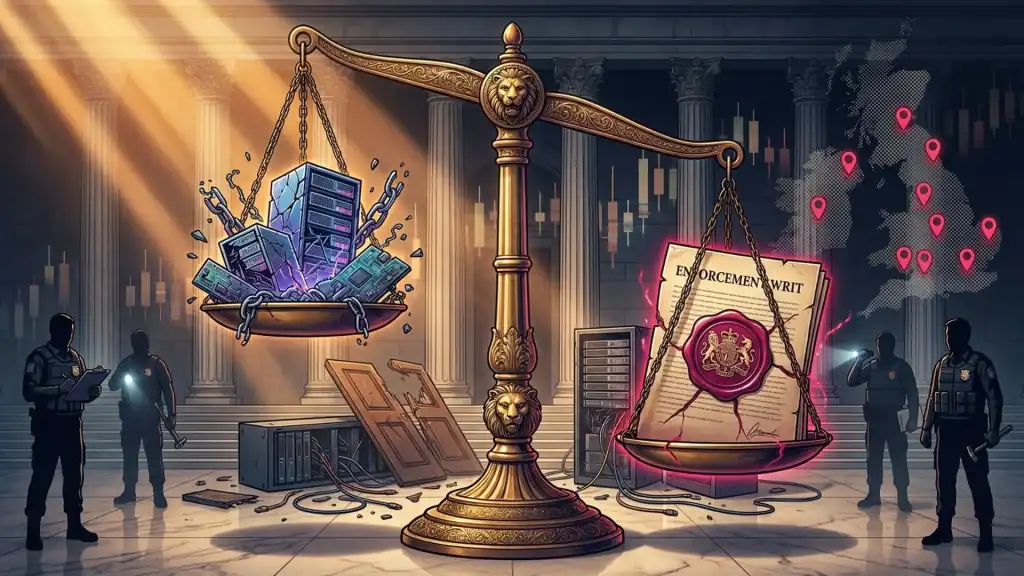

The Financial Conduct Authority kicked down doors at eight UK locations on Wednesday, handing out cease-and-desist notices to operators suspected of running unregistered peer-to-peer crypto trading desks. It is the first time the regulator has launched a coordinated sweep aimed squarely at P2P crypto. Agents from HMRC and the South West Regional Organised Crime Unit walked in alongside FCA staff, collected evidence for ongoing criminal probes, and told operators to stop trading on the spot.

Inside the Financial Conduct Authority’s First Peer-to-Peer Crypto Sweep

This was not a regulatory slap on the wrist. According to the Financial Conduct Authority, the eight inspected sites were suspected of operating outside the UK’s anti-money laundering registration regime, which has been mandatory for crypto firms since January 2020. Investigators moved in, paused activity, and began building case files that could turn into prosecutions.

The sting follows a pattern. UK authorities have already prosecuted operators running illegal crypto ATM networks and arrested people linked to unlicensed exchanges. Wednesday’s raids take that playbook and point it at the OTC corner of the market that has mostly flown below the radar until now.

Steve Smart, the FCA’s executive director of enforcement and market oversight, kept the warning short and blunt.

Unregistered peer-to-peer crypto traders operating in the UK are doing so illegally and pose a financial crime risk.

Why Does Peer-to-Peer Crypto Trading Get Regulators Nervous?

Peer-to-peer crypto trading is exactly what it sounds like. Two people, one wallet each, a direct swap of cash for Bitcoin or Tether without a centralized exchange sitting in the middle to check IDs. It is the oldest way to move crypto, and it remains a favourite route for anyone who wants to avoid leaving a paper trail.

In the UK, anyone running that kind of operation as a business has to register with the regulator under money laundering rules. The catch? The FCA confirmed on Wednesday that not a single P2P crypto trader or platform is currently on its register. Every desk running in the country right now is, by definition, operating outside the law.

That is a striking admission. It means the compliance gap is not a handful of rogue operators. It is the entire sub-sector.

- P2P desks often settle in cash, making physical premises raid targets

- Transactions skip the KYC layer that centralized venues enforce

- Stablecoin flows through OTC brokers are hard to trace across jurisdictions

- Regulators view these desks as bridges between clean and dirty money

The Iran Connection and OTC Chokepoints

Slav Demchuk, CEO of AMLBot.com, told reporters that Wednesday’s raids signal something bigger than a one-off enforcement action. Under the incoming Financial Services and Markets Act crypto regime, unregistered OTC desks stop being an AML paperwork issue and start being treated as unauthorised regulated activity. That is a much harder charge to defend against in court.

Demchuk flagged a specific worry: OTC desks are a consistent chokepoint for illicit flows, including what he called Iran-linked evasion corridors where sanctioned actors, locked out of regulated exchanges, use informal brokers to move USDT and BTC in and out of fiat. Take those desks offline, he argued, and you take a working sanctions-evasion pipe offline with them.

The framing matters because it reframes P2P crypto from a hobbyist activity into a national security issue.

Unregulated OTC brokers are one of the most consistent chokepoints in illicit flows, including Iran-linked evasion corridors where actors cut off from regulated exchanges use informal desks to move USDT and BTC in and out of fiat.

Operation Atlantic Set the Stage

The P2P raids did not come out of nowhere. Earlier this month, UK, US and Canadian authorities wrapped up Operation Atlantic, a coordinated March enforcement push against crypto fraud networks that was only unveiled publicly in April. The numbers were not small.

Agencies including the UK’s National Crime Agency, the US Secret Service and Canadian law enforcement and securities regulators identified more than 20,000 victims across the three countries. They froze over $12 million in suspected criminal proceeds and traced an additional $45 million in stolen crypto tied to fraud rings.

Read Wednesday’s raids in that context and the pattern is obvious. Western regulators are stitching the enforcement side together faster than the compliance side can keep up. P2P desks, ATMs, OTC brokers, offshore exchanges: every rail that sits outside the registered perimeter is now a target.

What This Means for UK Crypto Regulation in 2026 and 2027

The FCA is not acting in isolation. It is clearing the ground for the new UK crypto regulation framework, the FSMA crypto regime, which is expected to take effect in 2027. Firms will be able to apply for full authorization from September 2026. When the framework goes live, the bar rises from AML registration to full regulated-activity authorization, the same standard traditional finance firms have always lived under.

The regulator opened a consultation earlier this month on guidance covering stablecoins, trading platforms, custody and staking. That consultation, read against Wednesday’s raids, tells operators exactly what is coming. Register or be raided. The soft landing period is over.

Expect more sweeps before September. The FCA has effectively announced that it will clean the stage before the new regime walks on, and the cheapest way to do that is high-visibility enforcement that persuades unregistered operators to either get in line or shut down voluntarily.

If you are a UK crypto user who has relied on informal OTC desks for privacy or speed, the calculus just changed. Those desks are now enforcement priorities, not policy afterthoughts. The next knock on the door might not be a customer.

Frequently Asked Questions

What is the Financial Conduct Authority cracking down on?

The Financial Conduct Authority raided eight UK sites suspected of running illegal peer-to-peer crypto trading operations without AML registration. It worked with HMRC and the South West Regional Organised Crime Unit, issued cease-and-desist notices on site, and gathered evidence for ongoing criminal investigations into unregistered desks.

How does peer-to-peer crypto trading work in the UK?

Peer-to-peer crypto trading lets two people swap digital assets directly for cash or bank transfers, skipping centralized exchanges. In the UK, businesses running P2P desks must register with the FCA under anti-money laundering rules. The regulator says zero P2P traders or platforms are currently on its register.

What was Operation Atlantic?

Operation Atlantic was a coordinated March 2026 enforcement push by the UK National Crime Agency, the US Secret Service and Canadian law enforcement against crypto fraud networks. It identified more than 20,000 victims, froze over $12 million in suspected criminal proceeds and traced another $45 million in stolen crypto.

When does the new UK crypto regulation take effect?

The incoming FSMA crypto regime is expected to take effect in 2027. Firms will be able to apply for full authorization from September 2026. The framework covers stablecoins, trading platforms, custody and staking, lifting the bar from AML registration to full regulated-activity authorization.

This article is for informational purposes only and does not constitute investment advice. Every investment and trading decision involves risk. Readers should conduct their own research before making any financial decisions.

FCA finally moved on P2P but the notice only names eight sites. Any word on whether LocalBitcoins-style escrow platforms were included, or is this strictly non-custodial order book stuff? The press release was vague on the technical distinction.

classic regulator playbook. wait until volume moves offshore, then raid the remaining domestic players and call it a win

Been through this in 2017 with the China exchange ban and again with NYDFS going after Bitfinex. Enforcement sweeps like this usually push liquidity to Telegram OTC desks within a fortnight, not kill the trade.

cease and desist letters do nothing against self hosted nodes